QSIF Equity Long Short

Our view on the fund, the AMC, the strategy, the performance & the investment team.

IME's Review of QSIF Equity Long Short

| Fund Rating | Strategy Rating | Performance Rating |

|---|---|---|

Upgrade | Upgrade | Upgrade |

View on the Fund

We view QSIF Equity Long–Short as a differentiated proposition that functions more like a long-biased long–short strategy; akin to a **flexi-cap portfolio with tactical short positions**. This positioning is supported by Quant’s investment philosophy and systematic framework based on high-frequency analytics. However, given the limited operating history and evolving nature of the SIF structure, we maintain a neutral stance on the scheme at this stage. We prefer recommending investments in strategies where investment teams, philosophies and processes have stabalised, and there is a demonstrable performance track record - and accordingly recommend wait for SIFs to stabalise over 2-3 years prior to investing. That said, for investors keen on participating in SIFs - QSIF long-Short is potentially one of the superior offerings - given the strong quant background of the founder Sandeep Tandon.

Strategy

Flexi-Cap with Tactical Short

Fund's Strategy View

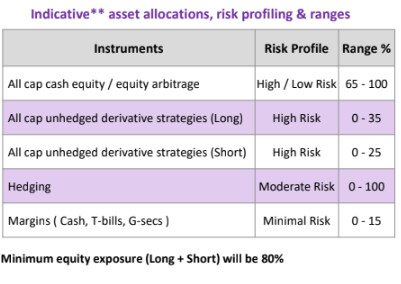

QSIF Equity Long–Short is a equity long–short strategy that maintains high gross equity exposure while actively managing net exposure through selective short positions (shorts up to 25%). The portfolio is constructed using Quant’s proprietary MARCOV framework, combining data-driven regime signals with discretionary oversight to determine long and short positioning. Long exposure is built through cash equities, equity arbitrage, and unhedged long derivative strategies (gross equity exposure ~65–100%, unhedged longs up to 35%), while short positions are used opportunistically to hedge risk, exploit weak or overvalued stocks, and smooth volatility (unhedged shorts up to 25%). Net exposure can vary from 55–100% (before accounting for hedging). Minimum total equity exposure (long + short) is maintained at ~80%.

Fund Performance

The funds aim to use shorts tactically to reduce portfolio volatility, downside protection during turbulent market conditions. Consistent ability to take such calls is key for low volatility returns over time.

Trailing Performance

| 1yr | 3yr | 5yr | Since Inception | |

|---|---|---|---|---|

| QSIF Equity Long Short |

Performance as of: 30-Jun-26 | Inception Date: 01-Sep-25 | Performance are post-fees, pre-taxes. Global funds denominated in USD or fund currency.

Investment team

Sandeep Tandon | 3-star rated FM

CIO | 30 yrs Experience | 19 yrs at current firm

Past Experience: GIC Mutual Fund (Trainee),IDBI Asset Management (Founding Member), ICI Securities, J.P. Morgan (JV), Kotak Securities, Goldman Sachs (JV), REFCO

Sandeep is the Founder and Chief Investment Officer of the Quant Group, he brings over 27 years of extensive experience in the capital markets. His remarkable journey in money management began in FY 1992-93 at GIC Mutual Fund, where he commenced as a trainee. Later, he became a founding member at IDBI Asset Management, contributing significantly to the establishment of the asset management business. He also worked at ICI Securities, a JV partner with J.P. Morgan in India, Kotak Securities, a JV partner with Goldman Sachs in India, and the former global derivatives firm REFCO.

IME's Review of QSIF (Quant)

| AMC Rating | Pedigree Rating | Team Rating | Philosophy Rating |

|---|---|---|---|

Upgrade | Upgrade | Upgrade | Upgrade |

View on AMC

We maintain a neutral stance on the SIF arm of Quant Mutual Fund. While the SIF structure provides access to more sophisticated and differentiated strategies, it remains relatively new and lacks a meaningful track record, warranting caution given the higher complexity and risks involved. Quant Mutual Fund itself is a niche, system-driven AMC with a clearly defined quantitative approach, a strong recent performance record, and an owner-managed structure. However, the platform remains highly dependent on Sandeep Tandon and follows a relatively aggressive investment style, making the SIF offering more suitable for investors with a higher risk appetite who are comfortable with limited operating history.

AMC's Pedigree

QSIF operates within Quant Mutual Fund, an AMC that has scaled rapidly over the past five years to over ₹90,000 crore in AUM by building a differentiated, system-driven investment culture. While the SIF platform itself is new, its pedigree is anchored in Quant’s long-standing focus on proprietary analytics and cycle-based investing.

AMC Team

QSIF’s investment team is heavily anchored in the expertise of Sandeep Tandon, who brings over 27 years of capital markets experience and has been a central driver behind the success and scale of Quant Mutual Fund

Investment Philosophy

At the AMC level, QSIF reflects Quant’s core philosophy of Systematic Active Investing, which blends structured, rules-based decision frameworks with discretionary oversight to stay adaptive across market cycles. The approach emphasises objectivity, continuous recalibration based on evolving data, and extensive use of proprietary analytics to dynamically manage risk and exposure, rather than relying on static views or rigid style classifications

Indicative Asset Allocation

Systematic Active Investing Framework

The investment process blends rules-based quantitative models with discretionary oversight, combining the discipline of systematic investing with the judgment of experienced portfolio managers.

Unlike purely discretionary or passive approaches, decisions are driven by data-based signals derived from price action, liquidity, market microstructure, and macro regimes, and are continuously recalibrated to adapt to changing market conditions.

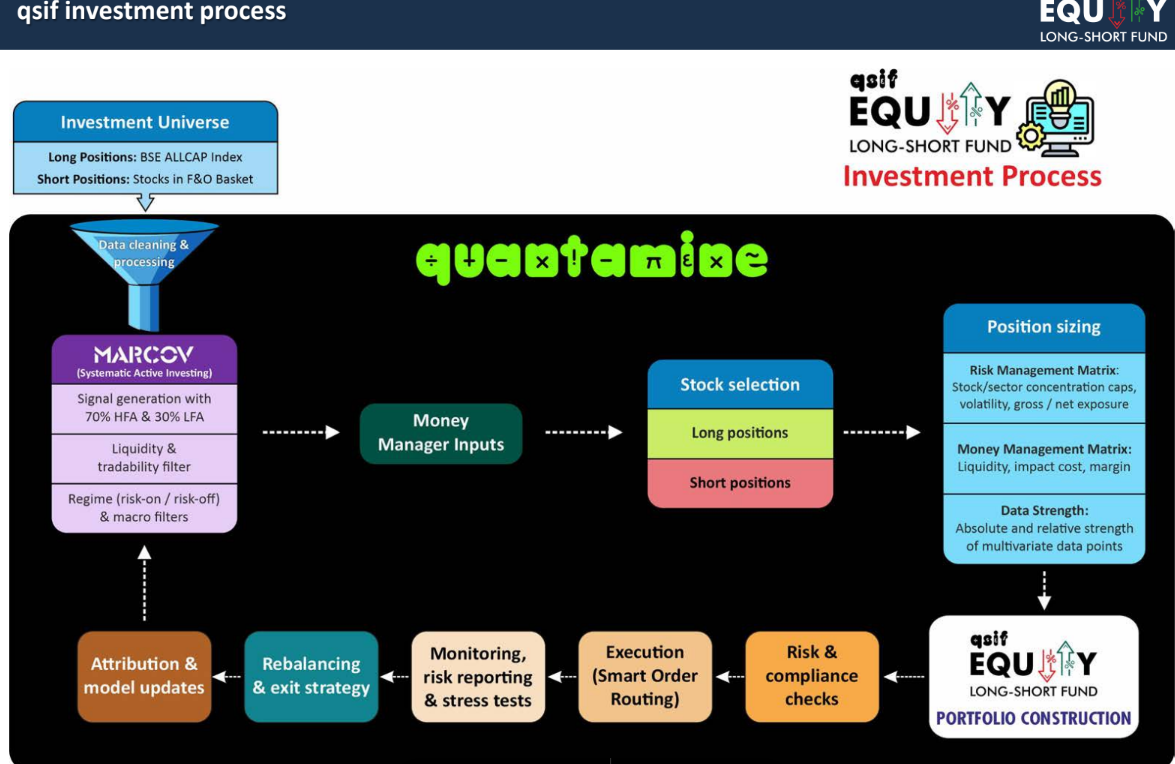

MARCOV – Proprietary Allocation and Risk Framework

This philosophy is implemented through MARCOV, Quant’s proprietary regime-aware allocation framework designed to optimize asymmetric returns while tightly controlling volatility and drawdowns. MARCOV integrates multiple analytical layers—market microstructure, alternate data, cycle analysis, volatility and risk metrics—into a unified decision engine.

High Frequency Analytics (HFA) and Quantamine Platform

A key differentiator is the use of High Frequency Analytics (HFA), which processes real-time data such as order flow, liquidity shifts, volatility patterns, and sentiment to identify early regime changes and risk inflection points. These capabilities are embedded within Quant’s quantamine platform.

Portfolio Construction

The portfolio is built as a flexi-cap equity book with a minimum 80% combined gross exposure (long + short). Long positions are aligned with favorable momentum, liquidity, and regime conditions, while shorts target securities exhibiting structural weakness or adverse behavioral signals.

Net exposure, gross exposure, and position sizing are dynamically managed using a structured risk framework incorporating volatility, liquidity, and stress testing.

AMC Background

Quant Mutual Fund originated as Escorts Mutual Fund, established in 1996 and registered with SEBI as one of India's earliest AMCs. In February 2018, Quant Capital Finance & Investments Private Limited acquired Escorts MF with AUM of ₹235 crore. Under founder and CIO Sandeep Tandon's leadership, the firm transformed from ₹135 crore AUM at March 2020 to ₹90,000+ crore.

Tandon founded Quant after 27 years in capital markets, including roles as founding member at IDBI Asset Management (where he conceptualized IDBI I-NITS 95), vice president at ICICI Securities establishing the equity derivatives desk, and stints at Kotak Securities, REFCO, and Economic Times Research Bureau. He was an early participant in India's Badla market and pioneered derivatives trading in institutional equities before launching Quant.

Investment Philosophy

MARCOV is Quant’s proprietary portfolio construction and exposure-management framework that combines high-frequency market analytics (~70%) with lower-frequency fundamental and macro inputs (~30%) to dynamically position portfolios across market regimes. The system ingests real-time signals such as price action, liquidity, volatility behaviour, order-flow patterns, and sentiment to detect regime shifts and market stress early, while the low-frequency layer provides broader macro and fundamental context. Portfolio allocations are model-generated but are subject to a human oversight layer, where money managers validate positioning before deployment. In long–short strategies, MARCOV actively adjusts gross and net exposure, shifting between hedged and directional stances based on market conditions, with longs typically drawn from the broader all-cap universe and shorts selected from liquid derivative-eligible stocks. The framework is designed to generate alpha through tactical long-short positioning while aiming to control drawdowns and reduce volatility relative to traditional long-only equity strategies.

Experience the benefits of working with a 'research-first' investments firm

Free 15-Day Trial of IME RMS App

Enjoy a complimentary 15-day trial of IME RMS and 3 1-hour consultations with a Senior Private Banker.

Access IME’s central research insights across MFs, PMSs, AIFs, SIFs and global funds, along with personalised support on risk profiling, mandate design, financial planning, and a portfolio review.

Experience the difference a research-first, transparent approach can make to your wealth journey.