Arbitrage Funds: Why Post-tax Yields are Superior to Debt Funds?

Post the change in taxation on debt funds from 1-Apr-23 (returns will now be taxed at your income tax slab, as compared to more favourable capital gains tax earlier), we have been recommending that investors consider Arbitrage Funds for their incremental fixed-income investments.

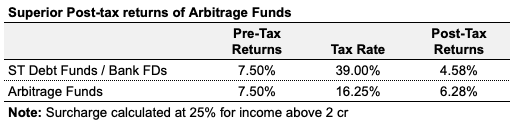

Arbitrage Funds offer Superior Post-Tax Yields to Debt Funds

Since arbitrage funds are taxed as equity funds, with a superior 20% short-term (less than 1 year) and 12.5% long-term (more than 1 year) capital gains tax rate.

Arbitrage Funds are very low-risk, with returns in line with market interest rates

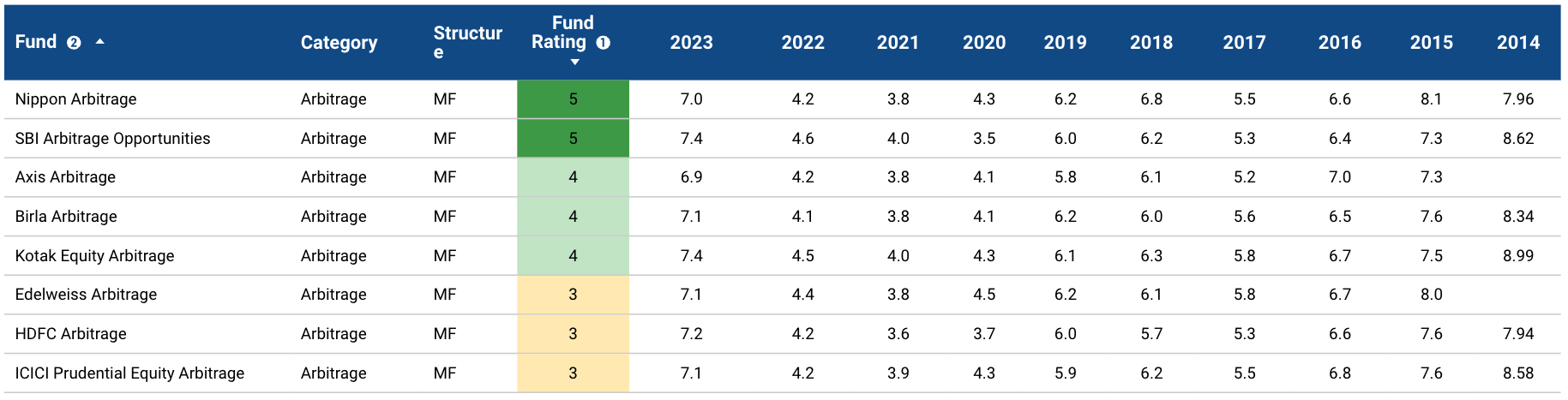

If you study the annual returns of various arbitrage funds (see table below), a few things are clearly apparent

-

Limited differences between arbitrage funds: Since arbitrage yields are driven by market interest, rates, most funds earn returns in a very similar range

-

Returns move higher & lower: Arbitrage returns are higher when market interest rates are higher, and move down when market interest rates reduce

-

Low risk-return: Arbitrage funds will neither give very high or negative returns, with their risk-return much more inline with low-duration debt funds

While Arbitrage funds have been in the Indian markets for decades, many retail investors are still unaware of how these funds work. We provide below a brief explanation of arbitrage transactions, and why arbitrage transactions & subsequently arbitrage funds are considered to be largely risk-free.

What are Arbitrage Funds

Arbitrage funds are funds that invest in risk-free transactions between the stock & the futures markets, with an aim to capitalize on price differences between a stock's future contracts and the underlying price of the stock.

Since these funds invest primarily in risk-free arbitrage transactions, their risk-reward is very similar to that of low-risk debt funds. The typical returns on arbitrage transactions, tend to reflect the underlying market interest rates for short-term lending (i.e. returns likely to be in-line with that of low-duration debt funds).

Understanding Stock Futures

A stock future is a contract to buy or sell a specific stock at a predetermined price on a future date. These contracts are traded on futures exchanges. The price of a stock future is usually based on the current price plus the cost of carrying or holding the stock until the contract's expiration date (this includes interest costs and minus any dividends).

The Stock Futures Price converges with the Stock Price on expiry

The settlement price of a futures contract on expiry, is equal to the closing price of the underlying stock on the expiry date. Therefore, regardless of the difference in prices of the stock & its futures contract before expiry, the two prices MUST converge on the expiry date (this is by definition, and there is no risk of this not occurring).

Why Stock futures typically trade at a premium to underlying stock

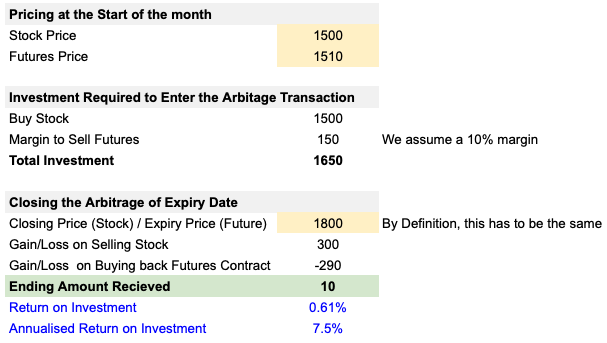

In normal market conditions, stock futures typically trade at a premium to the underlying stock, due to the inherent leverage that the stock future offers. For example, let us assume the price of Infosys is 1500 in the stock market. The futures contract (for an expiry one month from now), is likely to trade at a premium to this price (for example the futures contract may trade at 1515).

Both of these prices will be equal on the expiry date - accordingly as an investor if you want to buy Infosys assuming it will go up by the expiry date, you can either buy the stock (by investing Rs. 1500) or you could buy the future (this requires you to pay only a margin amount, which is typically 10-15% of the stock price. For example this could be Rs. 150).

By investing in a futures contract, you get essentially the same exposure as that of the stock, by investing a substantially lower amount of money (Rs. 150 as compared to Rs. 1500 for the stock). This technically is similar to your buying a stock, by investing Rs. 150 of your own money and borrowing the balance amount from a bank (for which you would end up paying interest - for example you may have to pay Rs. 15 interest for borrowing the money for 1 month).

The premium that stock futures contracts tend to trade at, reflect a market interest cost commensurate to the leverage that the futures contract is providing the investor.

Understanding the Arbitrage Transaction

Since a stock future typically trades at a premium to the underlying stock, an investor can enter into a risk-free arbitrage transaction, by doing the following transaction:

-

Start of Month: BUY (underlying stock) & SELL (futures contract)

-

Reversing Transaction on Expiry: SELL (underlying stock) & BUY (future contract)

-

Earn the Spread: Since the prices of the stock & the futures is the same on expiry (no matter whether the stock has gone up), the investor will essentially earn the premium that the futures contract traded at to the stock, at the start of the month

This transaction can be seen in the example below

Are Arbitrage Funds absolutely risk-free?

All investments carry some degree of risk, and while arbitrage funds are very low on the risk-spectrum (due to their engaging primarily in risk-free arbitrage transactions), investors should be aware of the following risks that can impact returns from Arbitrage funds:

-

Open-ended structure risks: Since arbitrage funds are structured as open-ended funds, any large redemptions at a fund level, that forces a fund manager to prematurely close out the arbitrage transaction can potentially adversely impact returns. The negative impact on returns takes place if the FM has to close out the transaction, before the spreads have compressed reflecting the holding period.

-

Spreads can decline in bearish market conditions: In bearish markets, the buying interest of stock speculators (who tend to be the primary buyers of stock futures) can be reduced. This can reduce the spread to below that of market interest rates (or in extreme cases, even lead to negative spreads).

-

Tax-Changes in the future: While returns of Arbitrage funds are similar to low-risk debt funds, they enjoy the more favourable taxation of equity funds. If the government were to change the taxation in the future, this tax-advantage could disappear (however based on past experiences, this is likely to only impact future transactions).

Are Arbitrage Funds right for you

Amongst low-risk fixed income investments, arbitrage funds offer what are currently the best post-tax yields for investors in higher tax-slabs. Their relevance in your investment portfolio, would be a function of your financial goals, investment mandate, tax-rates and your other such unique requirements. Learn more about whether you should invest in Arbitrage funds, by getting in touch with one of our investment specialists using the live Chat or appointment booking options on this page.

Experience the benefits of working with a 'research-first' investments firm

Free 15-Day Trial of IME RMS App

Enjoy a complimentary 15-day trial of IME RMS and 3 1-hour consultations with a Senior Private Banker.

Access IME’s central research insights across MFs, PMSs, AIFs, SIFs and global funds, along with personalised support on risk profiling, mandate design, financial planning, and a portfolio review.

Experience the difference a research-first, transparent approach can make to your wealth journey.